Its data provides an overview of European plastics production, conversion, consumption, and waste management, and includes an analysis of plastics production from non-fossil sources, and recycling technologies.

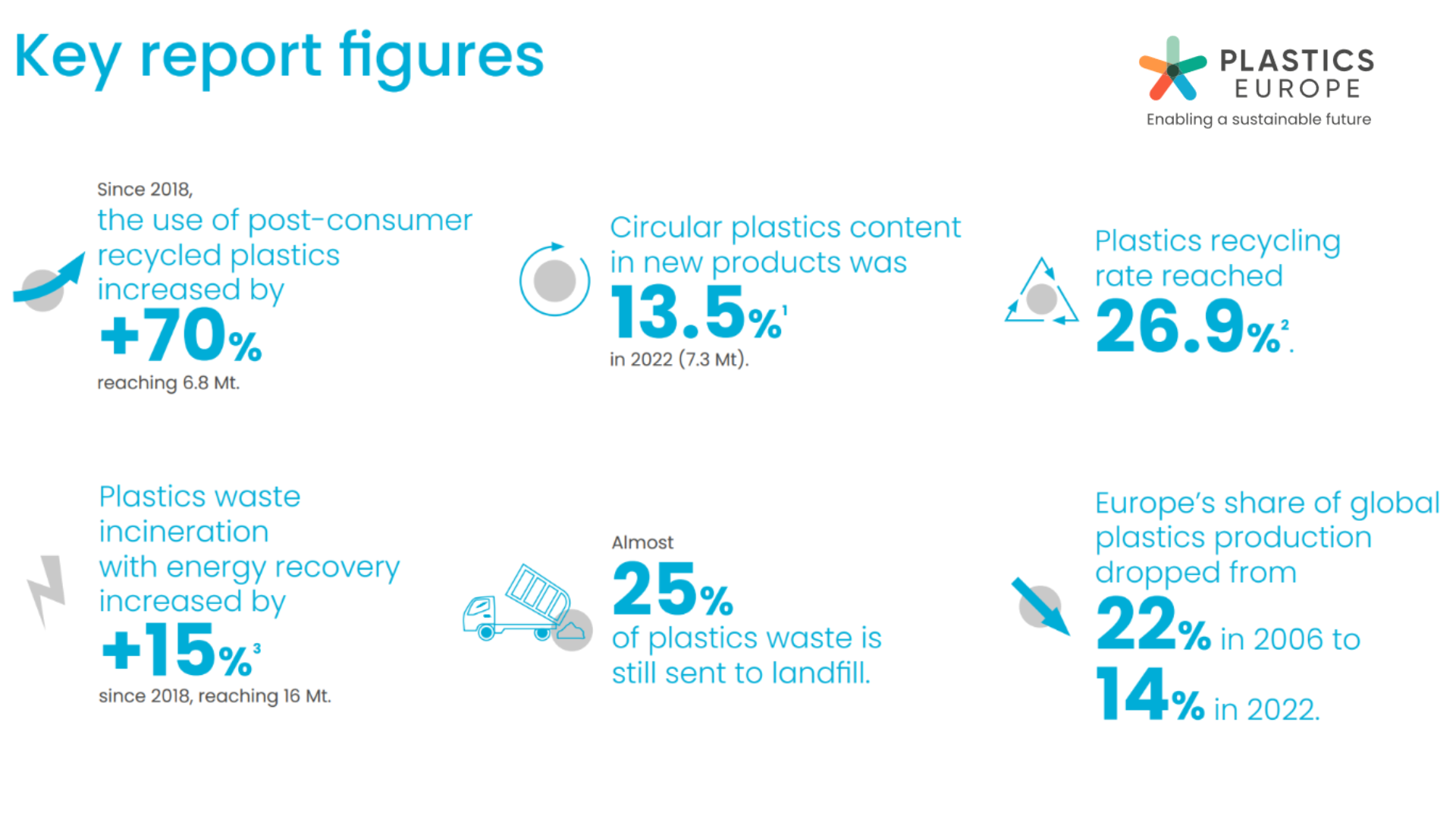

The study’s central finding is that circular plastics now account for 13.5% of new plastic products manufactured in Europe. This means that the European plastics system is halfway towards the interim ambition – established in the ‘Plastics Transition’ roadmap – to use 25% of plastics from circular sources in new products by 2030.

However, the report’s data also highlights several major challenges that will undermine the Plastics system’s progress towards circularity; including growing rates of incineration with energy recovery (+15% since 2018) of plastics waste needed as circular feedstock that could have been recycled.

Virginia Janssens, Managing Director of Plastics Europe, said: “Our latest ‘Circular Economy for Plastics’ report provides essential insights into the transition of the plastics system. This edition is also broader in scope and contains more in-depth data than ever before. Whilst the data confirms the shift to circularity is firmly established and picking up pace, it is frustrating that we still incinerate so much plastics waste when this potential feedstock is desperately needed by our industry to accelerate the transition. Without urgent action to increase the availability of all circular plastics feedstocks, we cannot maintain the current rate of progress and realise the ambitions of our ‘Plastics Transition’ roadmap and the EU Green Deal.”

In total, 26.9% of European plastics waste is now recycled, meaning that, for the first time, more plastics waste is recycled than is put into landfill; an important milestone in Europe’s plastics circularity journey. However, to meet the growing demand for plastics manufactured from circular feedstocks, we need to massively upscale the collection and sorting of post-consumer plastics waste, and increase the availability of biomass and captured carbon.

The data also highlights that the uptake of circular plastics is not uniform, but varies by industry sector. The strongest demand comes from the packaging, building and construction, and agriculture sectors, however others, including automotive and electricals and electronics, are falling behind.

The report found that in 2022 circular plastics were produced from several sources: the largest source (13.2% of all plastics produced) was mechanically recycled, while only 1% came from bio-based feedstock, and 0.1% was chemically recycled.

The report also shows that Europe’s share of global plastics production decreased from 22% (2006) to 14% (2022). If this continues, Europe will become increasingly dependent on imports and its ability to invest in circularity and support the transitions of the many downstream sectors and value chain partners that rely on plastics, will be undermined.